Most of us have an iconic and memorable first-time-on-a-bike story. Maybe your story starts with a slow-motion wreck in the yard but ends with a smooth sail down a hill, wind in your hair.

Think about what happened between the beginning and ending of that story, though. Somewhere along the way as you were learning to ride, you doubted your abilities because you fell or crashed or just didn’t get it. But you kept at it and eventually learned to ride.

And that’s how it goes with budgeting. As with any new skill, budgeting requires a little bit of practice and patience to get right. And we know you can do it! For most users, it takes about three months to go from novice to know-it-all.

If you’re brand-new to budgeting, we’re here to help! Follow our quick and easy guide below:

Month One

Your Goal: You’re no accountant (unless you are!) so go ahead and set your expectations accordingly. Make it easy on yourself and go through your bank statement from last month to set your housing, transportation and food costs. Doing this will give you a realistic starting point for tracking expenses. Give yourself a little room for error here. The first month is all about getting to know your budget and even learning to have fun with it.

Focus on This: With your budget made, do your best to stick to it. You’ll probably mess up this month and that’s okay. By tracking your transactions you can easily see the categories where you’ve spent too much or where you have money left over. Did you spend more on your grocery budget than you budgeted for? Adjust another category—like clothing or entertainment—to get your budget back to zero.

Month Two

Your Goal: Learn from last month. Remember the mistakes we said you’d probably make? This is how you make the most of them. You’ll use hard data from the past 30 days to adjust your budget and plan for the weeks ahead.

Focus on This: Determine where you overspent or underspent in the previous month and decide how you might fix these budget categories moving forward. Do you need to up your planned amount on groceries or find ways to lower your caramel latte intake? Make some tweaks (always ending up at zero) and see how your changes hold up to reality.

Helpful Hint: Maybe your Miscellaneous category lumped everything from a doctor copay to teeth whitening strips together. If you find that your “catchall” category includes too much, create breakout categories labeled Copays or Toiletries. There’s no limit to your line items.

Month Three

Your Goal: Move over amateurs, you’re about to go professional. For the past 60 days, you’ve tracked and tweaked your budget. Now it’s time to evaluate how you’re spending your money. In other words, it’s time to start shaping your budget around your goals.

Focus on This: Work your way through the Baby Steps. Do you need to pay off debt? Invest more in your retirement? Or save for a house? Consider smaller goals too, like saving for vacation or Christmas, a new car, or a home upgrade. Play around with your budget, starting with your highest priority and moving to your lowest. We always suggest budgeting in this order: giving, saving, necessities and then wants.

Helpful Hint: Look for areas where you can save even more money—like renegotiating your insurance premiums or shopping for generics over name brand. Once you start looking, you’re bound to find many more ways to save!

At the end of 90 days, you should be able to create a new monthly budget in just 10 minutes. Think about it: just minutes a month—and a commitment to sticking with your plan—could totally change the trajectory of your life!

A goal is a wish your heart makes . . . when you’re wide awake and ready to start getting life done.

Part of being an adult is realizing there’s no fairy “goal-mother” with magic dust who makes wishes come true—which is good, because it also means your dreams won’t turn into pumpkins at midnight. But it’s also bad, because it means you’ll have to work for them.

What are financial goals?

You’ve probably thought about other life goals: getting fit or healthy, becoming more intentional with your time, or learning a new skill. But what about money goals?

Think of where you want to be—financially—in the next five, 10 and 20 years. What about next year? Thinking about the big and small things is what you have to do when you’re writing out your goals.

And writing out you must. Goals are actionable dreams. So the first action step is to write them down. When you put goals into words and keep them in front of your face as both a reminder and a motivation, you’re beginning to bring them to life. So give them breath. Write them down.

How do you choose your financial goals?

But wait. How do you choose which goals to make your own? Where do you start? Start here—with our list of 10 financial goals. Read through and think about which ones best connect to your life and your dreams.

10 Popular Financial Goals

1. Create and stick to a budget.

When you get serious about your finances, you have to start seriously budgeting. Not only is this one of the top 10 financial goals people set each new year, it’s also the foundational goal on which all others should be built. If you aren’t budgeting—setting up a plan for all the money coming in and going out—you can’t gain momentum with your other money goals.

2. Build up an emergency fund.

Life happens. But you can be prepared for any money problems that come your way if you’ve got money saved up. When you have an emergency fund, you can rest well at night knowing you’re able to stand up against a financial threat without being beaten. You aren’t living paycheck to paycheck; you’re living with confidence. Those good vibes are better than any memory-foam, lavender-scented, lullaby-playing pillow out there.

This early ‘90s pop-dance tune reference is your friendly musical reminder that “debt hurts, debt scars, debt wounds and mars.” (That one’s from the ‘70s.) We’d parody any song out there if it meant encouraging people to pay off and then avoid debt. But we aren’t the only ones singing the praises of that debt-free lifestyle. Getting out of debt is a trending financial goal. And though many are still living on credit cards and taking out car and student loans, more and more people are realizing how much “debt stinks (yeah yeah).” (You knew we couldn’t leave out the ‘80s.)

4. Live on less than you earn.

The best way to get ahead is to stop getting behind. It’s not poetry. It’s not science. It’s common sense.

Getting ahead with your money is within your reach, but that calls for living on less than you earn. So what does that mean and how do you get there? It means more money comes in than goes out. Then you’re able to put some into savings and investments and start thinking ahead. (See how it’s all forward?) You also get there by becoming more intentional about your spending. Budget every month, find deals, use coupons, save to pay cash, and—super importantly—learn to say no, at least sometimes, to stuff that costs money.

And the easiest way to make sure you’re not spending more than you make is to create a plan for your money and stick to it—aka a budget. It’s easy to see why this one’s on a list of important financial goals. Spend less, and you’ll accelerate all your money goals.

5. Travel more.

Not all money goals are serious and stuffy. Some look really good on Instagram—like biking the streets of Amsterdam or eating croissants and taking selfies in front of the Arc de Triomphe in Paris. Is traveling one of your top money goals? Maybe you don’t want stuff as much as you want experiences, or maybe you’ve just always had the travel bug. Either way, start a sinking fund for the trip of your dreams, and you can make it come true—maybe even sooner than you think!

6. Save money to pay cash for big items.

Not only should you cash-flow travel, but you should also cash-flow big purchases. Cars, furniture, technology—these things cost money. Having dollar bills in hand to pay for these items—in full—is a fabulous financial goal. This puts you in the driver’s seat, steering yourself toward owning things rather than owing for things.

7. Stop living paycheck to paycheck.

Seventy-eight percent of Americans live paycheck to paycheck.(1) What’s that? Living paycheck to paycheck refers to a financial lifestyle with the stability of a parachute made of dandelion fluff. It means money in, money out: Each month pays only that month’s bills with no look to the future because you just can’t yet.

Hearing it broken down like that shows why people would want to end the paycheck-to-paycheck cycle. It’s a great financial goal to aim for! It means budgeting, as well as spending less and saving more. But it’s possible. Seriously. So consider taking this goal on and finding security like you’ve never known.

8. Pay off your home.

There’s no place like home. It’s where you sleep and eat and hang your heart. Also, it’s usually the largest expense in your budget. We specifically recommend 25% or less of your take-home pay. Imagine getting 25% of your income back to spread out over your savings account, travel fund, favorite charity, home-improvement bucket list, woodland-creature whittling hobby, and retirement account. That’s what happens when you pay off your mortgage. And that’s why this is a fantastic goal. The work is hard, but the payoff is immense.

9. Save up funds to help your children pay for college.

One of the greatest financial myths of today is that college isn’t possible without some debt attached. And it’s a doozy of an expensive myth at that. We disagree! Prospective students should go on intense scholarship and grant hunts, writing all the essays and filling out countless applications. And they should always consider in-state and community college options and—by golly—work throughout school to pay for tuition and fees.

We know parents often think about their kids one day dawning the doors of a great university—and they want to help pay for it. If you’re in this boat, know that navigating the waters of college savings funds isn’t as stormy a task as you may fear. Don’t feel pressured to make or meet this money goal, but if you’re financially able, helping your children pay for college would be an incredible blessing to give them.

10. Live your retirement dreams.

As you imagine your golden years, what do you see? Do you want to pack up an RV and see all of America? Do you want to read every book on your shelves you’ve been intending to for your entire professional life? Do you want to invest more time woodland-creature whittling? (Yes, we referenced it again. It’s a lost art.)

No matter what you envision this future looking like, you’re going to need money to make it happen. When you stop working, your income goes away. So having a financial goal in place to replace that paycheck with retirement investments is not only nice—it’s necessary!

Why is it important to set financial goals?

If you don’t set goals, things won’t change. You’ll stay right where you are—in the land of wishful thinking. And while that’s a fun place to have some thought vacations, it’s no place to live.

Financial goals give a voice and direction to your dreams. They give them shape, activity and life. Don’t kill your dreams. Instead, set financial goals.

How can you make it happen?

Write out your goals.

You won’t do them if you don’t write them, speak them, see them. So do it. NOW.

Create accountability.

Find someone you trust to talk through your goals with. This needs to be someone who can give you a reality check and encouragement along the way—someone who’ll check in on your progress and cheer on your accomplishments. Having accountability means you don’t leave your dreams on your own shoulders; you pick someone to help you carry the load.

Follow a solid plan.

If you look over that list of 10 financial goals, you might feel a little overwhelmed. Where do you start? What comes next when you decide you’re ready to make your money goal a reality?

We use what’s called the 7 Baby Steps as our guide in this situation. Walking this financial journey all the way to retirement is a long and winding road so you should take one (baby) step at a time. (See, that’s where the term came from!)

Budget.

For a budgeting app, we sure talk about budgets a lot. Funny how that works. But is this a chicken-and-egg situation? Do we acknowledge the power of budgets because we’re a budgeting app, or are we a budgeting app because we acknowledge the power of budgets? It’s both.

Don’t spend too much time worrying over which came first. Instead, sing this to the tune of Michael Jackson’s “Beat It” and feel inspired to “Budget. Budget. Then your dreams won’t be defeated. . . just budget. Just budget.”

Track your expenses.

No budget works if you set it up and leave it alone. That’s like adopting a puppy, buying it a fluffy bed, telling it not to chew up your shoes, and then leaving for work. That puppy’s going to chew up your shoes. And the rest of your house. It’s what untrained puppies do.

Once you’ve set up your budget, you still have to be attentive to your spending by tracking your expenses.

Keep your shoes unchewed and your spending in check. Train your puppies and track your expenses.

Become more self-aware.

While you’re trying to make these financial goals a reality, remember that your greatest cheerleader and opponent, hero and villain is . . . you. Socrates once said, “Know thyself.” Anyone who rocks both a toga and a ringlet beard must be pretty self-aware and self-secure. So in this case, listen to Socrates.

Know your money weaknesses and set up a plan to avoid or overcome them. Know your money strengths and build on them as you celebrate every victory (big and small). Plus, being more self-aware is one of the top keys to crushing any goal.

Reevaluate your goals every now and then.

Life changes. People change. Goals can change. That’s okay. Don’t abandon a goal just because it’s going to mean hard work. But don’t hold on to an outdated goal just because you don’t want to feel like a failure. Accepting that you’re heading in a different direction than you once thought isn’t failure. It’s actually healthy!

Reevaluate your money goals every year, every six months—and maybe every month if you’re into it. Never be afraid to make changes so these goals better suit where you are and where you’re going.

Goal diggers, you’ve got this. Seriously. Whether it’s a new year, a new month, or a random day and you’re feeling motivated to change—you’ve got this. Be intentional and get ready to work on making your dreams come true.

You’ve been plugging away for months creating zero-based budgets, logging your transactions, paying down debt, and saving up for emergencies.

Maybe you’ve been budgeting for years. Maybe this entire budgeting concept is completely new to you. In any case, if you’ve been working hard at crushing those goals, it’s time to reward yourself. You know what they say: “All work and no reward make for one burnt-out budgeter,” or something like that.

You might think rewards sound expensive. The truth is rewarding yourself can be expensive, but it doesn’t have to be.

Don’t neglect treating yourself just because you think your new budgeting lifestyle can’t handle it. There are plenty of ways to reward yourself that won’t bust your budget. And because you know we’ve got your back, we’ve come up with a solid list of thrifty or free ways to do just that!

Ways to Reward Yourself for $5 or Less

1. Stay-at-Home Movie Night

Going to the movies can add up quickly: tickets, sweets, popcorn, drinks. If you have kids, you’re adding in babysitting fees. If being in the actual theater for the release of a major film is your thing, there are plenty of ways to save on that expense. But there’s also a cheaper option—one you can enjoy on your own couch in your pajamas.

You can have a movie night at home for just $5. We can prove it:

One-night DVD rental ($1.50)

Two boxes of movie candy ($2)

Popcorn ($.50, if that!)

Two liter of soda ($1)

Not only will you save money, but you also won’t have to shush that chatty person sitting behind you in the theater. Plus, you can pause the movie for as many bathroom breaks as you desire.

2. Potluck Game Night

Invite your friends over for a classic game night. You probably have some good games stored away in that catchall hall closet, and you can rely on the resources of others for this too. Ask your friends to bring their favorites with them.

Plus, if you go potluck-style with the snacks, you’ll save even more. Real friends don’t mind bringing chips and salsa or their famous chocolate chip cookies to share in exchange for a night of competition and camaraderie. Spend that $5 on your share of the refreshments, and it’s game on.

Now, go back to your once-frequented shop, and reward yourself with an old favorite. As you sip the sweet, caffeinated goodness, think of how much better it tastes as a treat for your hard work rather than a taken-for-granted daily routine.

4. Dollar Store Shopping Spree

(Disclaimer: This one cheats just a little, so to cover the tax, raid that compartment in your car where you throw loose change.)

When was the last time you checked out your local dollar store? We’re talking about the everything-for-$1 kind. These places carry a lot of junk—but they’re also a treasure trove for smart shoppers.

Go in with your $5 plus those hunted-down coins and pick out five treats. A mug with a funny saying, candy, new sunglasses, organizational baskets, craft items, picture frames, donut-themed candles—these places are never short on thrifty fun!

5. Take a Hike

Some days the weather is so perfect you can nearly hear nature begging you to go out and enjoy it. We get busy and forget how much good some simple fresh air and outdoor exercise can do for us.

Search online for nearby hiking opportunities. The internet is a perfect place to figure out the hike’s location, difficulty and length. And a hike can cost you nothing, unless you want to buy some snacks or need a leak-proof water bottle (which is a great investment anyway!).

6. Free Near You

We’d all be surprised to see how much free entertainment we miss out on—just because we don’t think about it. Do a quick online search for upcoming local fun. And never forget the power of your library card. Cultural presentations, family and kid events, story time—you can find plenty to enjoy if you look around and think outside the fun-is-expensive box!

Ways to Reward Yourself for $10

7. Buy Yourself Something Nice (and Cheap)

We often get stuck in the rut of thinking nice things are always expensive things, but that just isn’t true. Think about things you love; then consider what you can purchase that would add to or upgrade this passion.

Writers: Buy a new journal and/or those perfect-ink-flow pens.

Runners: Purchase some new pump-up songs for your playlist or an audio book to listen to as you put in the miles.

Cooks: Buy that $10 kitchen gadget you’ve been eyeing—the one you don’t need every day, but you really want anyway.

Spa Enthusiasts: Invest in bath salts, bubble bath, a candle, and a mud mask. Turn on some relaxing melodies and soak up the goodness of meeting your financial goals.

Readers: Hardcovers aren’t cheap, but consider the electronic version of that book you’ve been dying to read. We have several e-books for just $9.99: you can put that extra penny back in your car’s random change bin.

Everyone: You get the idea! Be creative when you’re hunting down that little something extra to enjoy.

8. Go Camping—In Your Backyard

Has your entire family been working on these financial goals with you? You all should celebrate. If you have a tent and plenty of blankets, you could have a backyard campout. Hotdogs, buns, and chips aren’t too expensive, and if you hit the sales right, s’mores won’t bust your budget either.

If you don’t have a tent or don’t feel like sleeping outdoors, you can always pile up in the living room. Remember to tell the kids how proud you are of everyone’s efforts to be smart with money.

9. Go Where the Deals Are

When restaurants and entertainment centers realize they have a consistently low-volume night, they often get creative with their prices and promotions. This is when the budget-minded, night-out-loving person pounces. Check out local spots to see what they have to offer.

For example, how much ifs a bowling lane and shoe rental on an off night? We found a place near our office with a great Monday special. You could roll right into an awesome reward night if you’re willing to do some online searching.

10. Subscribe

We were surprised by how many magazine subscriptions cost $10 or less! This is the gift (to yourself) that keeps giving (twelve times, anyway). And each month your magazine comes in, you’ll have a happy reminder to keep rocking those money goals.

Just be sure to check your subscriptions a couple times a year to make sure you haven’t taken on too many. And don’t get stuck in a pricey cancellation policy or auto-renewal loop.

Making and sticking to a budget isn’t always easy. If your motivation to keep on keeping on falls by the wayside, it’s time to reward your awesome efforts. Introverts and extroverts, the competitive and the calm—anyone can enjoy a reward without wrecking all that good budgeting work.

You’ve started budgeting. Three cheers for you! This is a huge step—and the most important—in making those money goals a reality.

Maybe it’s going well. Maybe it’s hard. Maybe it’s somewhere in between. Wherever you are on the comfort-and-ease-of-budgeting scale, we’re always here for you. And we’ve got 12 solid tips at the ready to help the process run even smoother and the results get even better.

Take Your Budget to the Next Level With These 12 Tips

1. Budget every month before the month begins.

To get ahead, you need to think ahead. This is solid life advice—and a superb first budgeting tip. You need a new budget each month. And you need to set that up before the month begins.

It’s easy! You can copy this month’s budget to the next, and then adjust where you need to. Think about the unique spending coming up (like your BFF’s birthday or that yodeling competition entry fee) and move money around to make room for it.

2. Budget to zero.

Why? Telling all your money where to go means you’re in charge of it—you own it instead of the other way around. Practically speaking, here’s how you create a zero-based budget:

Add all sources of income.

Type in your fixed expenses, like mortgage or rent, utilities, food and transportation.

Then type in common monthly expenses, such as restaurants, entertainment and clothing. Check your past budgets or bank statements to get an idea of what you typically spend.

Give every dollar a name, meaning all your income has a place in your budget. If there’s still money left after you’ve entered all those expenses, put it toward your current money goal, like paying off debt.

3. Track every expense.

Seriously. Every. Single. One. The impulse pack of gum. The drive-thru coffee on the way to work. The corgi-covered socks. Those things add up. Literally. $ + $ + $ = $$$. Tracking every expense is how you know where all your money’s going. Then you can start telling your money to go exactly where you want.

4. Review your spending habits.

You have to get real with yourself. And you do that by reviewing your spending habits. That gum-buying routine, drive-thru coffee habit, or sock obsession could be costing you some serious money that would be way better spent on your current money goal.

Be honest with yourself about places you overspend. You either need to cut back or think about upping a budget line. But, remember, if you spend more in one spot, you have to spend less in another. It’s the circle of budgeting, young Simba.

5. Set a realistic budget.

Like we just said, it’s okay to add some money into a line if you’ve been unrealistic with the planned amount. If you’re trying to save on groceries, for example, and you’ve done all the coupon clipping, meal planning, and BOGO shopping you can—but you’re still overspending each month—you probably need to up that grocery budget.

But remember, there’s no magic money tree dropping dollar bills into your wallet when you change a planned amount. Like a teeter totter of money, when one budget line goes up, another must go down. Sorry, entertainment line: I need real food more than the mega-size popcorn at the movies.

6. Make adjustments.

So, as you see, adjustments will and must be made as you budget. Don’t freak. Lots of people think a budget is set and can’t be adjusted. But no way, friend. No way. This is your money. And you’re the boss of it. That’s what a budget does. It puts you in charge.

So we already said you’ll need to adjust when you realize you started with unrealistic expectations. You’ll also need to adjust when a bill is more or less than what you planned. Moral of the story is: Don’t be afraid to make adjustments. Just keep the goal of spending less than you make (overall) a key objective. That’s how you succeed with your money.

7. Create a “Miscellaneous” category.

We’re not elephants. We do forget. Your kid’s school fundraiser. Your $2 portion for that co-worker’s birthday cake. Your anniversary. (Yeah. Don’t forget that.) You might be surprised when these things pop up, but your wallet doesn’t have to be. Make room in your budget for the little things that slip your mind by creating a “Miscellaneous” line with $50 or so in it.

8. Budget for semi-annual expenses.

There are some things that really shouldn’t be a surprise hit to your budget, though, even though they don’t come every month. We’re talking about those semi-annual expenses like car insurance, your pet’s annual checkup, your anniversary (because—seriously, you should be ready for this). One perfect option is to set up a sinking fundfor any and every semi-annual expense. This way you can be saving up month by month for the day that expense is due.

9. Save for big purchases a little at a time.

Another great thing about sinking funds is you can use them to save up for big purchases. Be prepared for new tires by being watchful of the treads on all the wheels. Save up for Christmas all year long since you know it’s coming December 25. Pay cash for that new digital camera to take your photography hobby to the next level (or create a new side hustle). You do all these things by setting up sinking funds and setting aside money each month for that big purchase.

10. Budget for fun.

We don’t mean to budget for the fun of it—though we think budgeting is quite fun. We mean put in a budget line for fun things. All work and no play make you a dull, angry, frustrated, back-sliding budgeter. Of course, don’t go crazy. But there are ways to have fun and even reward yourself on a budget. And it’s easier to stay on track when the track offers one fancy coffee a month, extra foam, hold the guilt.

11. Understand the difference between needs and wants.

Speaking of fancy coffee—we all know that’s a want and not a need, right? Yes. We do. But other lines can blur. If your shoes are literally falling apart, you need new shoes. But that red vegan leather moto jacket—that’s a want. We budget for both, but needsget the priority.

12. Give yourself grace.

You will make mistakes. We all do. And it generally takes three months before you get the hang of this budgeting thing, so be kind to yourself—both at the start and throughout your new budgeting lifestyle.

Because that’s what this budgeting stuff is—a lifestyle. And it’s the best kind possible: the life doesn’t control my money—I DO! daily decision to make better money decisions.

You’ve got this. We mean it. You just need a“Yeah I can!”attitude and a budget.

*Don’t expect to start literally rolling in cash during your first few months, or even your first few years. That takes time. Scrooge McDuck didn’t build his money bin in a day, after all.

It’s time to talk about how to find contentment. Why? Because this important attitude can help you on your budgeting journey and in life.

What Is Contentment?

Contentment isn’t as much the buzzword these days as happiness, joy, or even gratitude. But it should be, because it encompasses them all and even goes one step further. Contentment is a feeling of fulfillment and satisfaction. This state of being may seem impossible in a world where everyone seems to want more more more. But it’s not.

By following these tips, you can learn to be more content. But remember: Contentment is a process. But sticking with it will be worth your effort.

4 Ways to Find Contentment

1. Express gratitude.

A grateful heart is a content heart. So make it a habit every day to think of at least one thing you appreciate. Maybe you could do this by starting your morning quietly with coffee and gratitude or ending your evening with thoughts of thankfulness. Maybe you could apply this to loved ones and be more conscious of giving compliments.

Express gratitude daily—even on bad days. There’s a good chance this practice will put some of those bad days into perspective. Except bad hair days. There’s no saving those.

2. Focus on what you have rather than what you don’t.

Getting caught in a cycle of want is easy. You look around your house thinking of all the upgrades you could do or stare in your closet dreaming of all the new clothing you could own—if only you had more money or a rich, gift-giving aunt. Right?

Wrong—meaning, this is the wrong way to think. It’s more than okay to have financial goals and dreams. (In fact, you should.) And it’s fantastic to make plans so those dreams come true.

But it’s not okay to let your focus on the future get in the way of any enjoyment in the present. Of course we aren’t saying you should overspend for a quick emotional burst of happiness. What we mean is—next time you look around—think more about what you do have than what you don’t.

3. Stop comparing yourself to others.

Though it’s not an Olympic sport yet, it could be soon because it’s incredibly popular. We’re talking about the comparison game. The problem is, everyone who plays this game loses.

Maybe that’s why they won’t bring it to Beijing in 2022. Who wants to watch a game where everyone loses? And yet—nearly all of us are willing to play.

Stop comparing yourself to others. Stop it now. No one has it all together. No one’s life is perfect. Those who seem to have it all could secretly be buried under a pile of debt. Why? Because they’re spending over their means while comparing themselves to someone else who seems to have even more.

It’s a vicious cycle and a fast-track to discontentment, which is the opposite direction you want to go. Pivot. There’s no chance for a gold medal here. Walk away from the comparison game for good.

4. Actively pursue the contentment mindset.

If you want to find contentment, you have to actively pursue the contentment mindset. Define what it looks like for you, personally. Then step into the journey of having more. Not more stuff—more satisfaction.

But how? You’re busy. And you don’t even know where to start.

We suggest you start with this simple journal. It carries a significant opportunity—the chance to be guided from the ease of living overwhelmed and unfulfilled to the beauty of living intentionally in contentment.

It is possible to reach contentment, but you have to be willing to take the first step. And then the next. And the next . . .

So put the journal in your budget. It’s more than worth it for this 90-day journey that’ll lead you through the process of becoming more grateful, humble and content.

Ever catch yourself counting down the days until your next paycheck?

Maybe you decided to take out a store credit card for the 20%-off shopping day and the bill just came in. Or maybe your “check engine” light is on and you’re dreading the repair. Either way, that paycheck can’t come fast enough—and might not be enough.

For 78% of Americans, living paycheck to paycheck is a way of life, an endless cycle of money going out almost as soon as it comes in.(1) Kind of like a revolving door you can’t exit, it keeps you from getting where you want to go. But it doesn’t have to be that way anymore. Here’s how you can escape for good.

1. Build an emergency fund.

One of the reasons it’s hard to get ahead is because life likes to throw curveballs when you’re prepped to hit a fastball. You can have a budget for all the expected things coming that month, but that doesn’t mean you’re ready for the unexpected.

You need $1,000 in a starter emergency fund so you can still get on base with your money instead of striking out every time life pitches you a surprise.

2. Create a budget.

We just mentioned that a budget is for all the expected things. It’s a tool that puts you in charge of your money, telling it where to go and what to do. Every. Single. Dollar.

You need to budget each and every month. It’ll be a little sticky and tricky to start, but after the first three months, you’ll get the hang of it. Soon you’ll be as good at budgeting as Meryl Streep is at acting. (Or maybe half that good, which would still be outstanding.)

3. Track your spending.

A budget with all theory and no action is completely useless. It looks pretty and all, sitting there in your app, but it won’t help you if you aren’t sticking to it.

Whether you’re new to budgeting or could get called up to the budgeting major leagues at any moment, this stick-to-your-budgetstuff can be challenging. But you’ve got this. We believe in you more than a kid believes that donkey with the cone on its head is actually a unicorn.

The way you stick to your budget is by tracking your spending all month long—every expense, every income, every time.

4. Save for big purchases.

A big reason we tend to get stuck in the paycheck-to-paycheck cycle is because we’ll make a huge purchase on a whim. That means we say yesto a beach vacay with friends the month-of or buy a new laptop when we want an upgrade. These in-the-moment spending habits drain the month’s budget. It’s no good to get ahead with stuff—or even awesome experiences—if it means getting behind with your finances.

We aren’t saying you have to say no to all big purchases. We’re saying you have to think ahead, plan ahead, and save ahead! Use the sinking fund method: Figure out how much an item or experience will cost and save up bit by bit over a period of time. With your EveryDollar budget, you can set up a fund in mere minutes.

When you save up for big expenses, you can enjoy the stuff without the stress.

5. Rethink your wealth-building tools.

Wealth-building tools may bring to mind a red box filled with hammers, screwdrivers and pliers. But those aren’t the tools you need to build wealth. To build wealth you need money—and good sense on how to use it.

Your biggest wealth-building tool is your income. So spend some time thinking about your career. Do you feel like you’re in the right job? Is your salary appropriate for the work you do? Are you doing the right type of work for your skill set and talents?

In his latest book, author and career expert Ken Coleman shares that 70% of Americans are disengaged at work.(2) Maybe your paycheck-to-paycheck living is rooted in the problem that you’re in a job you don’t love. When you feel like you’re working with purpose and meaning, it’ll change your entire attitude about the money you bring home.

No matter your age, your background, or your income—you can get in control of your money. You need an emergency fund, a budget (that you stick with!), a new pattern of saving up before you spend big, and a job that helps you build wealth and gives you a feeling of purpose.

Ah, snap. Things were going so nicely. You felt like you had your life together. And then . . . it happens. It meaning your water heater busts, your car manages to get twoflat tires, and you crack a tooth . . . why?

Thankfully, you had an emergency fund. Unthankfully, now you don’t. It feels good to pay cash to fix the problem, but then your emergency fund is drained—and now what?

Now, you go all Rocky Balboa on it and run up a bunch of stairs chanting, “It ain’t about how hard you hit. It’s about how hard you can get hit and keep moving forward.” Meaning, you rebuild that emergency fund.

There’s no shame in that game. This is what the fund is for—emergencies. It did its job—and well—so get back on those stairs and show life you’re going to keep moving forward. You will rebuild your emergency fund.

How to Rebuild Your Starter Emergency Fund

The starter emergency fund is $1,000. We call this the first Baby Step in our money goal journey of 7 Baby Steps. If you’re rebuilding this emergency fund, you can do some or all of these five tips.

A couple may seem a little intense, but remember, this is for a short time to get that $1,000 back in action for the next financial bump in the road of life.

1. Make a budget.

If you aren’t already on a budget, you need to be. It’s the best tool to realize where your money is going so you can start planning where you want it to go. And right now, you want a good deal of it to be going into savings, right? Get on a budget so you can make that happen.

2. Track your spending.

To make a budget work, you need to track your income and expenses—everything that comes in and goes out. This way, you’ll know if you still have money in your restaurant budget line to join your friends in celebration of National Burrito Day and, of course, if you’ve got enough to spring for guac or queso.

3. Pause other money goals (Baby Steps).

So, you’re busy punching debt in the face. You know we love that. Paying off debt with intensity is our jam. We call it Baby Step 2.

But if you’ve got to go back to Baby Step 1 to fill up your emergency fund once again, pause the debt-punching intensity. Pay the minimum payments on all debt only until your savings is back at $1,000. Then, let the fists of financial fury loose on your debt once again.

4. Go on a short-term spending freeze.

You can make this one as challenging—aka as long—as you’re willing. Try a day of zero spending or a week (maybe even a month) of no superfluous—aka unnecessary—spending.

Be your own barista, wear those old wedges, make a marvelous movie night at home. Gather up all the money you save by not spending on these extras and take it to the bank. Literally.

5. Cut out some extra expenses.

There are some spots in your budget that are a little . . . fluffy. One of your three TV streaming services (the one you haven’t logged into in months). Your superhero sock of the month subscription box. The maid service. Restaurants. (Don’t hate! We aren’t saying to never eat out again! It’s short-term, friends.)

Gut the fluff. For now. You might even realize you don’t miss some of it.

How to Rebuild Your Fully Funded Emergency Fund

If you’ve had a much bigger expense hit and you need to rebuild what we call Baby Step 3 (a fully funded emergency fund), you can use any of the tips above and some below as well.

Since a fully funded emergency fund is a storehouse of savings for 3–6 months of expenses that can keep you afloat in case of a big emergency, like job loss, you’ll be working on this longer and may want to take bigger measures.

1. Sell stuff.

You’re probably surrounded by things you don’t really use: an extra television, a surplus sofa, unused electronics. Get selling. Go online to places like Craigslist, Poshmark, ThredUp or your local selling page on Facebook.

Or dust off those folding tables and make some signs for a good old-fashioned yard sale. If you’ll sell off some of that excess, you can clear out the clutter in your life and earn extra cash to stash back into your emergency fund.

2. Find a side hustle.

If you need more money, make more money. Get yourself a side hustle, aka an extra part-time job. Delivering pizzas used to be about the best, quickest, easiest way to do this. Now, it’s one of many simple options.

You can also pick up delivery jobs for Amazon Flex, Uber Eats, Grubhub, Postmates, Shipt, or a grocery store near you that offers food delivery services. Uber and Lyft are good if you love driving and love people. Oh, the conversations you’ll have and, oh, the interesting people you’ll shuttle around.

And don’t forget about all the ways you can profit from your talents. Tutor, give music lessons, babysit, pet sit, dog walk, or design birthday invitations. People are paying for these services—they might as well pay you! You can rebuild your emergency fund quickly, and maybe you’ll discover you want to keep the side hustle to point that extra income toward other money goals.

3. Save on groceries by meal planning.

You can cut a quick $100–300 off your monthly grocery budget line with one simple tip: meal plan. Yes, it takes some work. After all, it’s called meal “planning” and not meal “showing up on your table without effort.” But that extra hundred or three a month is no joke.

Just like your budget gives all your money a job, meal planning gives all your food a job. When you make a meal plan, you’re buying only what you need for the week. It keeps you accountable to yourself when you’re walking by all those beautiful endcaps in the grocery store with promises of delicious snack times and lunches your kids will tell all their friends about on the playground.

Make a meal plan by mapping out what your family will eat all week for breakfast, lunch, dinner and snacks. Save even more by planning these things around what’s on sale that week at your favorite grocery store. Make a list. Check it twice. Then, shop that list—and don’t veer off of it.

Grocery shopping isn’t a Sunday drive with no place to be. Don’t take a side road. Stick to the list. Your wallet will thank you—at least a hundred times.

4. Cut the cable.

The average household spends $1,237.20 a year on cable TV.(1) You’re probably not going to go radical, drop the cable, and not pick up any other television options. But you could trade in cable for a much lower-priced streaming service—like Hulu, Netflix, Amazon Prime Video, YouTube TV, Sling TV, and the list goes on.

Even if you pick up two of those options, you’ll save around $90 a month and still have tons of television entertainment available to you and yours.

5. Consider downsizing your home or apartment.

Whoa. Did we go too far with this one? Hang with us a moment. We aren’t saying you should move your family of six to a one-bedroom apartment. But give this idea of downsizing (or down-pricing by moving to a different neighborhood) some thought.

When we talk about budget percentages, our suggestion for the housing category (rent or mortgage, HOA fees, insurance, and PMI) is no more than 25% of your take-home pay. If you’re spending more than that or if you’re right at this amount but would love to free up lots of money in your budget, a move could be the way to do it.

It might mean giving up some amenities (do you even use that puppy spa?) or that second bonus room (the one that collects all the stuff you’re planning on selling in the next garage sale anyway), but it could also mean quickly rebuilding your emergency fund and gaining a huge peace of mind with your finances.

6. Switch to term life insurance.

If you have a whole life insurance policy, it’s time to switch to term life. Why? Many, many, many reasons.

We’ll cut to the chase, though. First of all, you pay on a whole life insurance policy for, well, your whole life. That means that, after you’ve invested and saved well to retire well, you’re still paying on an insurance policy you don’t even need anymore because your gorgeously plump savings and investments are your insurance now! No, thank you, whole life.

Secondly, term life is a better financial deal. Whole life costs about $300 more a month. That’s a quick $300 to put into rebuilding your emergency fund. And when the emergency fund is back in action, that’s an extra $300 to throw at saving up for retirement, paying off your mortgage early, or setting up a college savings plan for junior.

That $300 a month turns into $3,600 a year and $108,000 over 30 years. Gasp. Go switch to term life insurance right now.

7. Know it’s okay to say no.

Oh, the power of the word no. We should all exert this power more often.

Should I have a third helping of that chocolate molten lava cake with a side scoop of vanilla ice cream? No. Should I get a perm and tease my bangs? Surely that ‘80s hairstyle will make a comeback. No. Should I buy these tickets to the polka rock music festival? It’s not really in my budget, but . . . No.

Enjoy that first helping of cake, leave that ‘80s hair where it belongs (in the past), and don’t spend money outside of your budget.

Listen, we know that the budget feels a little tighter than usual when you’re trying to rebuild your emergency fund, so you’ll be saying the magic word no more often than usual. But that’s okay. It’s for a season. And what you’re really rebuilding here is security against what could come and empowerment over your money.

That’s worth any season of being scrappy or sometimes stingy with your money.

In the olden days, marriage began with a herd of goats, a small ceremony with a minister to make it official, a prim church organist banging out “Canon in D,” and maybe a potluck to celebrate the nuptials. But today, marriage begins with more pomp and circumstance. In fact, it’s a giant to-do—which comes with a giant to-do list.

Far from a chore, though, your wedding can be one of the most memorable and special days of your life! But before you jump all in to the Pinteresting, planning and prepping, you need to pause and take these four solid steps forward.

Four Steps to Take Before You Start Planning Your Wedding

Step 1: Determine the type of wedding you want.

Are we talking indoor, outdoor, destination, church, old train station, old train caboose, castle on the coast, White Castle? If you’re wavering at all, start your guest list. That calculation could dictate the location. You can’t fit 500 friends and family members in a woodland treehouse wedding.

Of course, one of the quickest ways to save is to limit your guest list. But maybe tons of people celebrating your big day is your number one wedding wish. That brings us to the next point.

Step 2: Resolve your nonnegotiables.

As a couple, communicate with each other—tell each other what you want out of your wedding day. What are your top three most important wedding dreams? Food, flowers and filmography? Live band, location and lavender tuxedos?

After your top three have been decided, think about what’s not important? Keep your most valuable and most trivial items at the forefront of your minds as you begin to take the third, and biggest, step.

Step 3: Budget for the wedding of your affordable dreams.

That sounds sort of . . . um . . . unromantic. Huh? It shouldn’t! Starting a life together is beautiful. But starting the union off by draining a savings account or going into debt to impress yourself, your friends or your family—now that’sunromantic. Instead, give your budget a realistic number that still includes everything you want out of your big day.

Step 4: Have the budget talk with family.

In the past, etiquette dictated the distinct payment roles of the parents of the bride and groom. The couples were usually young and had little funds of their own to contribute. But this is 2018, when people are waiting later to marry and often paying for their own wedding. These days parents tend to pay around 46% of the wedding costs.(1)

You’ll need to have a conversation with your parents about their role in your wedding. And remember, they don’t owe you that trip to Jukkasjärvi, Sweden, in November to wed in the ice hotel before it melts into a mere memory. But if they’re willing to help out, it’s good to know how much they want to contribute from the start.

These days, the average wedding (including honeymoon and engagement ring) costs $36,000.(2) That’s a whole lot of money. If $36,000 sounds like a solid investment to you, then keep reading. You’ll see how to put all that to the best use. If $36,000 sounds impossible, keep reading. We’ll share plenty of tips to show you how to have a sensational celebration for less.

That’s right! This is wedding budget central, straight from your favorite financial friends. Because before you say “I do” to the rest of your lives together, you’ve got a lot of other I dos to figure out: I do want the chocolate-mousse-filled, cherry-ganache-covered cake with fondant orchids, or I do want our recessional music to be a duet between bagpipes and banjo.

We’re not saying all your decisions will be grand—but they will be yours.

What are your main wedding budget categories?

On average, 42% of couples underestimate how much money they need for their wedding.(3) That means they must suddenly scramble to find money they weren’t planning to look for. Don’t let this be you! Prep now so you don’t pay more later.

As you start to account for all the dollar amounts, you can use our Wedding Budget Planning worksheet. It divides your spending into these main categories:

We’re going to break down each of these, sharing some average costs as well as important things to consider. Remember your nonnegotiables as you read. And keep in mind you don’t have to spend the average amount we listed. Allocate more if something is top priority; budget less on things that aren’t as important to you.

Are you ready to set a budget you can both have and hold? Let’s get started.

Venue Costs: Where the Magic Happens

Average Cost: $9,000 Suggested Budget Percent: 20–25%

Location

The venue tends to be the first thing couples search for, usually around 11.1 months before the wedding. And the location of the ceremony and reception takes up about $9,000 of that $36,000 budget. (4)

When you’re booking your venue, consider the impact the month and day make on the location’s cost. Spring weddings used to be all the rage, with pastel pantsuits a plenty, but that trend has been taken over. Fall ranks at the most popular season for ceremonies with October as the most popular month.(5)

Busy venues know they can charge more when their services are most desired. If you’re willing to get married in January or February, the two least popular months for weddings, you should look or ask for a discount.(6) Your dream venue wants your money in non-peak months, and you want your dream venue. It could be a win-win for both of you.

Saturdays are the busiest wedding days, with Friday and Sunday coming in second.(7)Changing the day of the week could mean lower costs. You’ll have to remember that weeknight weddings might make it difficult for guests (especially traveling ones) to attend. It also means extra days off if you need to prep anything beforehand. And you could be seeing a lot more “declines with regrets”on those RSVP cards.

Wedding Ceremony Costs: The Moment That Starts a Lifetime Together

Average Cost: $3,900 Suggested Budget Percent: 8–12%

Officiant

Find out what your state requires to make your marriage official. Some call for much more stringent specifications than others. If you hope for a friend or family member to perform your nuptials, it may be possible. Just know your guidelines. And while some officiants charge and some do not, cash or a small gift as a way to say thank you is always a good idea. After all, their signature will sit on your marriage license for all time.

Music

Ceremonial tunes average $600.(8) If having a four–string quartet is crucial, you’ll pay that or more. But what about all those super talented friends you have? The ones who could have a music career if they applied themselves and knew the right people? Yes. Them. What if you asked them to perform your favorite love songs. How personal would it be if the processional was the first song you two held hands to—sung by your college roommate. Not the tone-deaf one—the one who can float through those vocal trills like Christina Aguilera. You could save money and create a more individualized moment.

Flowers, Lighting and Décor

Decorative elementsrun an average of $3,000 for the ceremony and reception combined.(9) That’s a lot of petals, twinkle lights, and draped tulle. Some venues have enough charm on their own, but most couples like to spruce up the place and add personal touches.

If you’re limiting your spending in this category, think about what will show in photos during the ceremony. A wooden arch decorated with greenery and flowers to frame the happy couple is probably a better investment than elaborate centerpieces. That arch will set a scene that you’ll be showing your great-grandchildren when you leaf through the photo album, while the centerpieces are just wow factor for the day.

Décor isn’t the only floral need. Most weddings use bouquets, corsages and boutonnieres. Maybe you want a flower girl to sprinkle rose petals down the aisle. That costs money. Maybe the guys don’t want boutonnieres. That saves money. Maybe you’ve dreamed of hydrangeas, calla lilies, or tulips for the bouquets—these spring and summer blossoms will come at a high price for your winter wedding.

This category is a major DIY-able zone. You don’t even need a florist: Check out the floral department at your local warehouse store or even supermarket. With any wedding project you want to take on, remember to consider the cost of supplies and how stressed you’ll get making it happen. Create everything far, far, far ahead of time so you aren’t hot-gluing paper petals (made from the sheet music of your favorite Beatles love song) into an elaborate bouquet the night before you wed. No one wants tired eyes and burned fingers in their wedding photos!

Reception: After the Vows, It’s Time to Party

Average Cost: $8,350–10,950 Suggested Budget Percent: 20–30%

Catering

We mentioned before that the venue is the most expensive item in most wedding budgets. And coming in second place is . . . drumroll please . . . oh, you probably guessed it: FOOD. Catering costs come up to around $6,600.(10) So, if you subtract the price of the engagement ring and honeymoon, which we’ll discuss later, from the average wedding cost, that means you, your family, and your friends will be eating 24% of your wedding budget.

That also means food is a fantastic place to get frugal. If you’re wanting a full meal, you can trade the sit-down, plated, four-course option for buffet style. You won’t be alone going that route: 54% of couples let guests fill their own plates.(11)

Having an earlier ceremony with a luncheon reception is another great way to save on your food budget. Maybe a midday meal is the way for you. If you want to save even more, offer just appetizers, dessert, or both!

Note that some venues will dictate your caterer, either because they have their own or have an agreement with another company. An all-inclusive event space could save you money and time, so keep this in mind when looking for your venue and your caterer.

The Cake

Speaking of dessert—let them eat cake! After all, according to Julia Child, a party without a cake is just a meeting. Do you want a tiered wedding cake and a manly groom’s cake? Just one cake? Cupcakes? A donut wall? Milk and cookies? We won’t tell Julia Child if you break from tradition.

But since love is sweet, offering some kind of sweet is, well, sweet. Having a small buffet of homemade treats versus a traditional three-tier wedding cake is a great way to save cash.

Flowers and Décor

Flowers and décor are a consideration at the reception as well. You could ask a couple of groomsmen to move some decorations from the ceremony spot to the reception venue. It’s highly unlikely your guests will gasp and exclaim, “Can you believe they moved those rustic wedding mason jar lights from the aisles to the centerpieces? How paltry!” For one, no one uses the word paltry anymore (sadly). For two, they’ll either not notice or assume you just have your wedding act together. Using décor twice is a clever way to save money!

About 77% of receptions happen indoors,which means you’ll have some sort of lighting already provided, but you may want to ramp up the ambiance with spotlights or twinkly string lights.(12) You can also consider renting some of your décor, purchasing pre-loved décor from online marketplaces like Facebook or Etsy, or buying things you could use in your home or as gifts to people after the wedding is over.

Music

Peace and quiet is a goal of retirement, not your wedding reception. You need some kind of music. Everyone loves music, but certain people are crazy about it. Some relationships are formed on this shared enthusiasm. If that’s you, we bet you made the jams at your reception one of your three priority-spending nonnegotiables.

A live band can cost $3,800. You could also hire a DJ if you want classic and modern hits to get people dancing. That costs far less at $1,200.(13) Both create a completely different ambiance—so once you figure out what you want, hire what you need. And if you want to get really thrifty, consider creating your dream playlist and plugging in to your venue’s sound system. Then you won’t have to worry about “YMCA” playing unless you want it to.

Beverages

Beveragesare a must. If your wedding is more DIY, you can go the water, soda, iced tea direction. If you’d like, you can offer your favorite beer and wine or have a champagne toast. This customizes the wedding experience and saves you from having to offer an open bar.

If your venue includes an open bar, even better. Many venues build beverages into their per-person price. If adult beverages are important to you, an all-inclusive venue may be the way to go.

You don’t want to leave your guests thirsty, but what you offer should be far more about the vibe you want to build balanced with the budget you’ve already built.

Photography and Videography Costs: Capturing the Moments on Film Forever

Average Cost: $4,200 Suggested Budget Percent: 6–10%

Engagement Photos

He said, “Will you?” She said, “Yes!” And it’s time to announce. What better way than with engagement photos?In fact, many guys hire someone to film or photograph the moment the question is popped! When you’re searching for the perfect photographer, consider one who includes engagement photos in their wedding packages. It’s a great way for the photographer to get to know you as a couple, as well as learn what you want from photos before the big day.

Ceremony and Reception Photos

You obviously want the actual ceremony photographed. From the walk down the aisle to the groom’s face as he sees his bride to the first kiss as husband and wife—all of these need to be captured. Many couples pay to have the reception photographedas well, or at least portions of it. And because these photos last a lifetime, the photographer is usually the fourth highest expense at $2,400.(14)

To make sure you get the most memories captured for your money, carefully look over package options. Some photographers work by the hour, which means you’ll want to have a list ready with all the family and wedding party pictures you want. The photography assistant, your wedding planner, or a firm and direct friend can keep everyone moving in a timely manner from one shot to the next. Whether or not your photographer is hourly, you don’t want a frustratingly slow photography process. You have a party to get to!

Videography

Not only do you want still shots of your wedding moments, you probably want your ceremony filmed, and maybe the reception filmedtoo. Whether you’re looking for a basic recording of the event or an elaborate movie-like experience, videography is a hot-ticket item these days averaging $1,800.(15)

Photo Booths

Photo boothsat weddings are becoming incredibly popular. These generate entertainment for your guests, up the numbers on your wedding hashtag, and offer a free (to them) memory for friends and family. You can save money by using an automated camera that emails or texts images rather than printing.

You can save even more by not offering this at all. You could just set up a playful selfie station with props and décor so your guests can use their phones to fill their social media accounts.

A photo booth isn’t expected, but is a fun addition if you’ve got the funds.

Attire Expenses: What to Wear to the Wedding

Average Cost: $2,900 Suggested Budget Percent: 5–8%

Bridesmaids Dresses

Oh, the jokes about bridesmaid dresses. Watch any 90s sitcom, and you’re bound to enjoy at least one moment of a leading lady lamenting over having to wear the ugliest frock ever fashioned. In the past couple of years, that trend has thankfully tanked, and a new one is on the rise: The bridal party is wearing different, yet coordinating dresses. About 59% of weddings support this wardrobe movement.(16)

But who pays? Generally, the bridesmaids buy their own dresses, which added another level to the hideous dress joke. Not only was it ugly, it was expensive. And even if you got to wear a fabulous frock, it wasn’t something you could ever wear again. What a waste!

Yes, this is your wedding. Yes, these are your choices. But when you ask your dearest friends to be a part of it, that privilege shouldn’t come with a giant price tag. There are multiple economical options such as renting, watching for sales, picking out a dress online, or buying pre-owned.

If you do jump on the multi-dress bandwagon, you can have final say in the selections, but it gives your gal pals a chance to pick out something in their financial comfort zone that they can wear again.

The Wedding Dress

What’s a wedding without a wedding dress?Shopping for this gown is a pivotal moment in a girl’s life. Saying yes to the dress (and posting about it on social media) is a must. How much does that yes cost? An average of $1,700.(17) Some of you nodded your head at the reasonability of that number. Some of you did a literal spit take with whatever you’re sipping on as you read this.

The dress is important. Seriously. As we said before, the photographs are what last forever, and guess what you’re wearing in those photos? Your wedding dress. But you might be surprised at how you can rival the beauty of a royal wedding dress for way less.

Don’t feel stuck going to bridal shops. Any formalwear store will have options in white. Look online or go to consignment stores for used dresses, either from unsentimental or runaway brides. If that feels weird, look for vintage versions on Etsy.

The dress isn’t all the bride needs to think about. Veil or no veil? Converse or couture heels? Pearls or diamonds? Remember not everything has to be brand-new. Maybe you buy the dress but wear your mom’s veil and his grandmother’s jewelry.

Let your style that day reflect who you are—and what your budget allows.

Beauty Services

Beauty servicescan range from having hair, nails, and makeup done to far more complex beauty rituals. We understand that if you have two left hands and can’t even get your hair into a pony tail you probably need some professional help getting picture perfect. Or do you? What about that friend who has a knack for painting nails or the half-cousin who does hair for fun?

We said it before, and we’ll say it again (probably again and again): Ask those friends who are talented to share their talents for a discounted price or in leu of giving you a gift.

Attire for the Groom and theGroom’s Party

It’s time to suit up. Or tux up. That’s one of the first decisions. Just as girls are wearing less matching and less formal gowns, guys are often going more causal as well. But whichever you pick, remember the men usually pay for their rental, so don’t make them get decked out in tails, silk bow ties, ruffle shirts, top hats and canes. All that costs extra. Always be thoughtful of the costs involved.

The groom’s attirerelates to his groomsmen. And the formality might relate to the venue. Are you going tux or suit? The benefit to the latter is you might be able to grab something that could be purchased and used again for other fancy affairs.

But renting a tux or suit is fairly common, and one of the lowest expenses coming in at $350.(18) In fact, that includes shoes and whatever accessories are needed (maybe the bow tie and suspenders, but not the cane and top hat—you’re not Mr. Peanut).

Rehearsal Dinner: Practicing and Eating Together

Average Cost: $2,000 Suggested Budget Percent: 4–6%

The night before the wedding, the couple, family and wedding party generally do a run-through finished off with a rehearsal dinner. The cost of this pre-wedding event is about $2,000.(19) That can cover the food, venue and beverages.

Some venues will give you location and food, and some need a separate caterer brought in. Don’t forget the power of someone’s house, your friend’s backyard, or your church’s fellowship hall and loads of BBQ for this evening together. You’ll still have a good time without the expenses tallying up.

Wedding Bands: With This Ring, I Thee Wed

Average Cost: $6,800 Suggested Budget Percent: 11–18%

Engagement Ring

If you ask people to guess the average cost of an engagement ring today, you’re going to get quite the range. The answer? $5,000.(20)We’re not here to tell you what you can and cannot spend on a piece of jewelry that goes along with one of the biggest questions you’ll ask in your entire life. But keep two things in mind when you’re opening that ring box to the words, “Will you marry me?”

Do not go in debt to buy an engagement ring. Set a budget, start a fund, and save up cash. You’re supposed to be walking into a shared financial future together: Don’t start on the wrong . . . knee.

Remember the proposal is about marriage—a life together—not a ring.

Wedding Rings

The exchange of wedding bandsis part of the ceremony. His and her rings average $1,800.(21)Many people look for bands that coordinate with her engagement ring, but this doesn’t have to be the case. Get something that suits your personality. That doesn’t have to be pricey platinum or a gold band.

Silicone rings are on the rise. These bands began as a safer option as they are easy to remove in case of an accident, but they’ve become popular with people who work out, work with their hands, or work in dangerous career lines such as firefighters or police officers. This isn’t the only nontraditional option for couples. Shop around.

Stationary: This Just In—Someone’s Getting Married!

Average Cost: $560 Suggested Budget Percent: 1–2%

Save the Date

The general public’s incredibly busy lifestyle (or an incredibly clever paper marketer) has made save-the-date announcements a must. While it’s great to get your ceremony on everyone’s calendar, you don’t have to spend money here. Consider joining the 36% of couples who send their save-the-date via email.(22)

Wedding Invitations

Invitations, with RSVP cards included, are the next stationary expense. And don’t forget the stamps, both for what you send out and what comes back. It’s quite common for the RSVP envelopes to be labeled with your address and a stamp for convenience. These days, plenty of couples save money by asking for text or online responses.

You want the invitation to speak to your style, perhaps giving a hint of the coming event’s vibe. But don’t spend a ton of money here. Except for your grandparents, parents and BFF—no one keeps these.

Programs sharing the day’s sequence of events aren’t as common these days. You’re more likely to see a wooden pallet or chalkboard with flourished hand lettering. If that’s an alluring alternative for you, put it in your flowers and décor budget and save paper.

Thank You Cards

The final paper you need to worry about are the thank you cards—which call for more stamps. Of course, you can shake a hand and share a verbal thanks. You can send an email or social media shout-out. But none of that compares to physical, handwritten thank you cards to people who spent their time and money to congratulate and celebrate your love.

You don’t need to spend hundreds getting cards that match your invitation. You can save money by going to a dollar store and grabbing a few twelve-packs. Or consider a personalized postcard. It’s the heartfelt thought that counts here, not the cost.

Transportation: You’ve Got to Get There

Average Cost: $1,000 Suggested Budget Percent: 1–3%

If you rented a limo for prom, you’re probably feeling like you need one for this far more meaningful formal event. You’ve got to get from one spot to another, but you don’t need to weaken your wallet to show up in style. Of course, not all vehicles can take your entire bridal party (if that’s something you’re needing) from the chapel to the reception. You may need to rent something sizable. Research local charter buses, trolleys, and limo services. Depending on the size of the vehicle and the time of day, week, year—you might be able to get something affordable and functional with just the right amount of flash.

And if drifting slowly down from heaven in a hot air balloon is one of your nonnegotiables, then this is one of the bigger budget lines for you. That’s all fine, as long as you’re keeping in line with your budget.

Wedding Coordinator: Because Someone Has to Keep It All Together

Average Cost: $1,700 Suggested Budget Percent: 4–10%

Some of us have a calendar with each day’s events planned down to the hour, a meal plan schedule for the rest of the month, and a binder with tabs for each of these listed categories. If you love to plan, you probably don’t need a wedding coordinator who plans from day one to day of. But you might want someone who tells people when and where to go on your wedding day: where to get their pictures taken, when to begin walking down the aisle, when to start playing “I Feel Good” by James Brown at the exact moment you are pronounced husband and wife.

This can be someone you hire or that friend or awesome aunt who lives that organized life we mentioned above. This category’s a balancing act. You don’t want to spend absurd money for services you don’t need, but the bride and groom shouldn’t be giving anyone tips or direction on their big day!

Gifts and Favors: Wrapped Thank Yous

Average Cost: $1,050 Suggested Budget Percent: 1–3%

Wedding Party Gifts

A good wedding party does more than stand beside you as you promise forever. They’re there to help when you need them, through planning the event and getting ready. A thank you in present form is no requirement, but it is considerate.

Wedding party giftsare usually a reflection of the relationship or something to use during the wedding, such as jewelry or a wedding-themed bow tie. Any bridesmaids, groomsmen, flower girls, ring bearers would fall into this category.

Wedding Favors

Wedding favorsare also quite common, but shouldn’t break your bank. They are a token of thanks, a remembrance of the day, a symbol of the new unity formed. They are not a chance to keep up with what everyone on social media and Pinterest says they’re doing, but should be a personal reflection of you as a couple.

Accommodations: Getting Out-of-Towners A Place to Stay

Average Cost: $800 Suggested Budget Percent: 1–2%

Out-of-Town Guests

Do you pay for any out-of-town guests to have accommodations? Yes and no. No because you shouldn’t have to. Yes, because you may want to pay for certain guests who travel in, like parents, grandparents, or even the wedding party. Or you can work with a hotel to negotiate room blocks for a discounted rate. This is purely your decision. There’s not etiquette you’re breaking in any instance.

Wedding Party

If you do decide to spend the night with your wedding party in a luxury hotel suite, you need to be up front about who is paying for what. When you plan to split the bill, that’s just between you, your future spouse and your budget. If you’re asking them to get in on the cost, be conscientious, like you were with their attire. Not everyone’s as excited to plop down thousands for your big day as you are.

Paperwork: It’s Not Official Until the Government Says It Is

Average Cost: $275 Suggested Budget Percent: 1%

Marriage License

Here’s a fee many forget to fit in: the marriage license. This formal piece of paper is what makes your marriage legally binding. You need one. The cost can range from $10 to $115, depending on your state and sometimes even your county.(23) In Tennessee, you can get a discount if you complete premarital counseling, even if it’s a free service offered by your minister!

You’ll need to apply for the license a couple days before the wedding—going in together with valid identification. You’re given the paperwork you need to get signed on your wedding day and sent off quickly. You’ll receive an official license in the mail. But you don’t want just one copy. Order extras! Why? Read on.

Name Change

If you’re one of the 70% who decide to change their last names after getting married, your (paper)work has just begun.(24) You’ll need to apply for a new social security card(which is free if you go through the Social Security Administration), passport (around $110), and driver’s license (around $50).(25) You need to change your name with your bank and job; You need an updated library card and aerial yoga membership id—and all these people want to see, you guessed it, a copy of your marriage license. Since you’ll be mailing it off in some instances, it’s easier to have more than one rather than wait until it returns or risk losing it in the shuffle.

However, here’s a pro tip: If your passport is less than one year old, you can get an updated copy with your new name at no cost! (26) If this applies to you, don’t dawdle and miss out on that savings opportunity.

Not only does changing your name cost money you might rather spend on tickets to see your favorite band, but it also takes oodles of extra effort. Try to keep basking in that post-marriage bliss as you’re sorting through websites and signing checks to one government agency after the other. (Hey. You’re signing your new name. That’s fun!)

Honeymoon: The Vacation After the Event

Average Cost: $4,000 Suggested Budget Percent: 8–11%

The honeymoon can range from the ultra-luxurious to the ultra-chill. When you’re planning, think about these three things: your couple personality, your time-off allotted, and your budget.

Do you love to go, go, go and experience new things? You may want to see a new country and party on a cruise (which can actually be as calm or crazy as you want it to be). Are you happiest when you’re together in the quiet? Book a cabin in the woods and bring a stack of books.

Be reasonable with how much time you take off work. You might have used a couple days for the actual day, especially if you were saving money by having a weekday wedding. Leave some vacation days open for the rest of the year. You’re a couple now, which means two sets of families to think about for every holiday. Life’s about to get double busy, so make sure you don’t plunder all your paid time off.

If you don’t have a lot of money to enjoy the vacation of your marital dreamsright after the wedding, it doesn’t mean that day will never come. In fact, we believe it will, as long as you’re willing to get yourself into a financially sound space first.

Save money on your honeymoon by looking for deals. Stay three nights, get the fourth free. Find mid-week or non-peak season specials. In fact, if a particular honeymoon destination is one of your top nonnegotiables, you might want to set your wedding date to align with your vacation visions. You may want to scale back on all the other items in the budget and focus your spending on the first trip you’ll take together as one.

Miscellaneous: For What You’re Not Thinking of or Planning For

Average Cost: $1,800 Suggested Budget Percent: 5%

Go ahead and plan 5% of the budget for anything you might forget! If you don’t end up spending this, put it in savings or treat yourself to something extra on the honeymoon.

Final Ways to Save Money on Your Wedding

We’ve mentioned some of these throughout, but let’s do a quick roundup of the overarching ways to save.

Ask friends or family to help in place of giving you presents. (See—we told you we’d say it again!)

DIY when you can—but make sure you aren’t stressing yourself to the point of not enjoying your big day. And don’t DIY when it would be cheaper in the long run (time and stress and costs included) to hire someone else.

Don’t book the first vendor you find—for anything! Compare prices and don’t be afraid to negotiate better rates!

In the end, the best advice we can give, beyond making and keeping your budget, is to remember the wedding is about you—and not about impressing or entertaining others. Communicate clearly and constantly together about what’s important and what’s not, and you’re on your way to the wedding of your dreams.

So how much does a wedding cost? The short answer is $38,700.(1) The long answer is thirty-eight thousand seven hundred dollars.

But what does that include? What should you be prepping to pay for the most magical day of your entire life?

The list of possible wedding costs has as much length to it as the train on Princess Diana’s wedding dress. Let’s unveil a few of them.

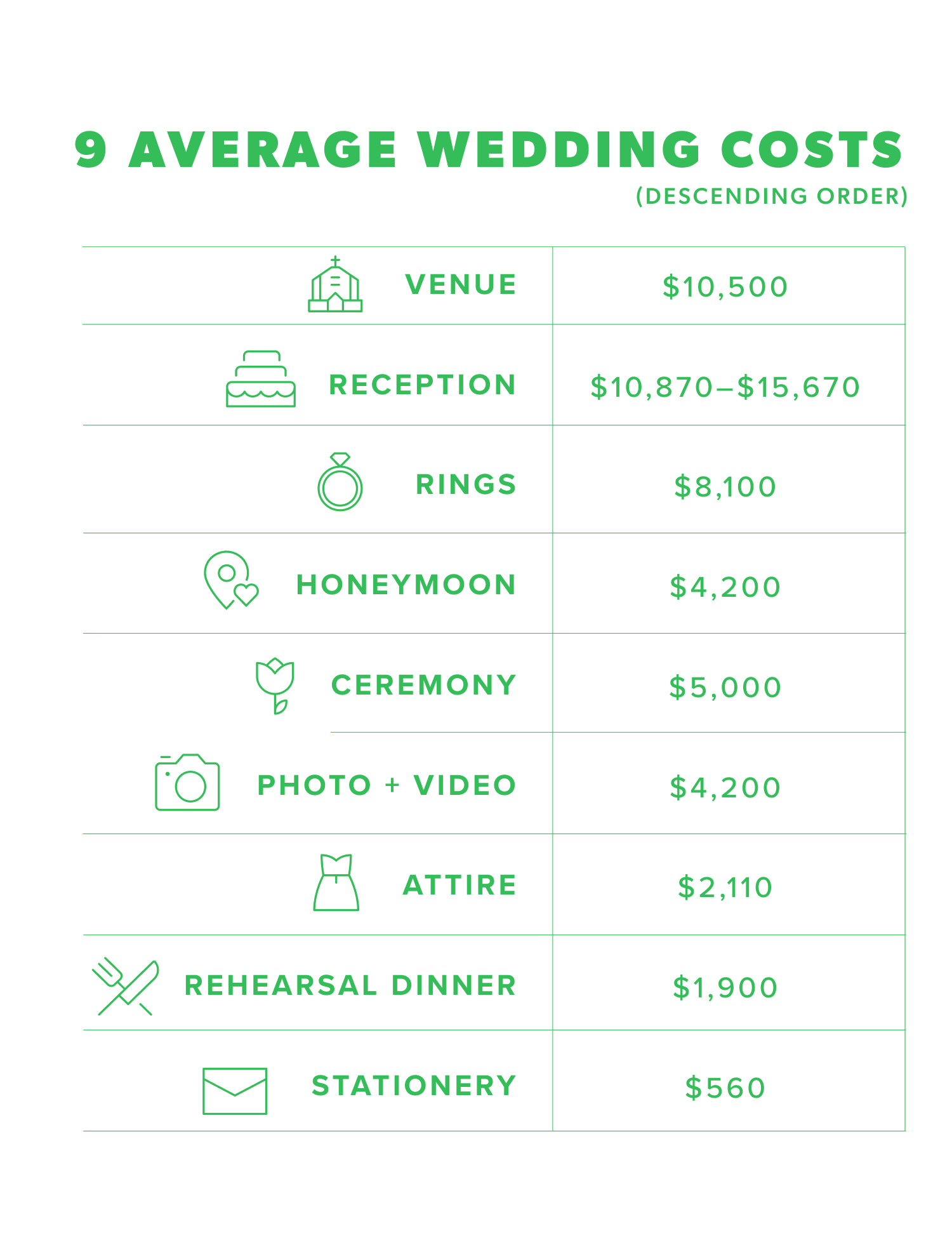

9 Average Wedding Costs

All average costs in the chart above and information below come from the WeddingWire research report.(2)

1. Venue

The venue is generally one of the largest expenses for a wedding. At a whopping $9,000, it takes up 20–25% of an average American wedding budget. Of course, you can save money by having your wedding on a less popular day of the week or month of the year.